| Penalty-Proof Your Tax Return Adjust your tax withholding now to boost your take-home pay or to avoid underpayment penalties when you file your 2010 tax return. By Mary Beth Franklin, Kiplinger.com When you file your tax return each year, the amount of tax withheld from your paycheck or submitted through estimated quarterly tax payments ideally should match the amount of tax you owe. In reality, that seldom happens. Most Americans are addicted to tax refunds, as evidenced by the fact that the average income-tax refund rose again this year to a record of nearly $2,900. In essence, more than 75% of U.S. taxpayers gave Uncle Sam an interest-free loan. Many of the remaining taxpayers ended up owing money, and some had to fork over an extra 10% penalty for having too little tax withheld throughout the year. Both situations are easy to remedy, but you have to act before the end of the year. Just file a revised Form W-4 with your employer. The more "allowances" you claim on the W-4, the less tax will be withheld; the fewer you claim, the more tax will be withheld. You can also ask your employer to withhold a flat amount from your paycheck. If you regularly get a refund, you've already banked most of it and will still get a refund next spring. But you can stop the leakage from your last few paychecks of the year by adjusting your W-4 now. Worksheets that come with the W-4 will help, or you can struggle through the IRS's online withholding calculator. But we've got a better idea. If your current financial situation is similar to last year's, just use our Tax Withholding Calculator. Answer three simple questions (you'll find the answers on your 2009 tax return) and we'll estimate how many additional allowances you deserve -- and even show you how much your take-home pay will rise starting next payday, if you claim the allowances on a new W-4. (However, this shortcut won't be much help if your tax situation has changed since last year because, for example, you have a new baby or got a new job). On the other hand, if you expect that you'll owe money when you file your 2010 tax return next spring, you can avoid an underpayment penalty by boosting your withholding now. You needn't pay every penny of the tax you expect to owe. As long as you prepay 90% of this year's tax bill, you're off the hook for the penalty. Or, you can escape its reach, in most cases, by prepaying 100% of your 2009 tax liability. (But if your 2009 adjusted gross income topped $150,000, you'll have to prepay 110% of last year's tax liability to avoid a penalty, even if your 2010 tax far exceeds your pay-ins.) If you have both wage and consulting income and expect to owe money on your tax return, boost the taxes withheld from your last few paychecks rather than trying to make up the shortfall with your final estimated quarterly payment due January 18, 2011 (because January 15 is a Saturday and the following Monday is a federal holiday). Taxes that are withheld are treated as if they were spread out evenly throughout the year, sidestepping an underpayment penalty; the estimated-tax-payment approach does not. Reprinted with permission. All Contents c2010 The Kiplinger Washington Editors. www.kiplinger.com.

--------------------------

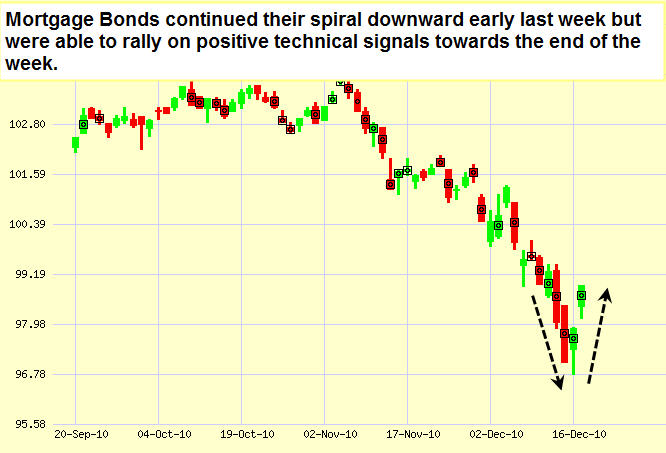

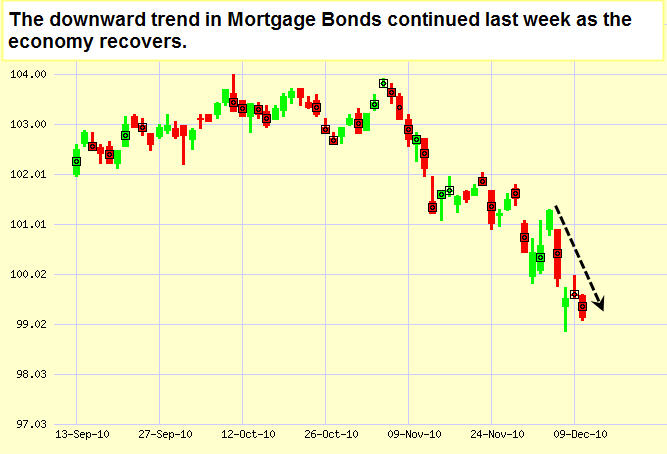

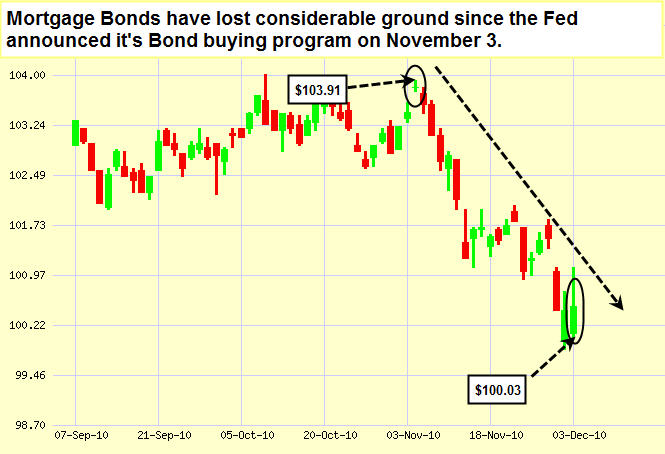

Economic Calendar for the Week of December 6-10, 2010 Remember, as a general rule, weaker than expected economic data is good for rates, while positive data causes rates to rise. Economic Calendar for the Week of December 06 - December 10 |