| In This Issue... |

|

|

| Last Week in Review: Europe and the Treasury Department impacted Bonds. Find out what it all means to home loan rates. Forecast for the Week: This week will be busy from start to finish... but the biggest news will hit on Friday. Read below to learn why. View: Mobile phone banking is convenient. But is it safe? Read these tips to help lower your risk! |

| Last Week in Review |

|

|

| "It’s not a matter of IF, but WHEN!" That old adage proved true last week as the fiscal problems in Europe came back to roost as predicted - even after being overshadowed recently by news from Japan and the Middle East. Despite all the focus on government debt in Europe, it’s important to note that the problems are more than just financial; there is also a ton of political capital at risk. The stronger and more fiscally conservative Euro member countries like Germany and France do not want to pick up the tab for poor performing countries like Ireland, Greece, Portugal and many others standing in line behind them. And as news flows out of Europe - either good or bad - Mortgage Bonds and home loan rates here in the US will move in sympathy. In fact, we’re already seeing it as Producer Prices (which look at wholesale inflation) are running at very hot levels... with prices up 3.3% in just the last three months. If pricing pressures don't recede for producers of goods and services, companies will have one of two choices: Either: Absorb the higher cost of goods - and, thereby, hurt earnings growth Or: Pass those increased costs onto consumers - thereby, creating consumer inflation Both of those scenarios would be bad for Stocks and Bonds. And since home loan rates are tied to Mortgage Backed Securities - which are a type of Bond - those scenarios would also be bad for home loan rates. Speaking of Mortgage Backed Securities, last week the Treasury Department announced it is going to begin selling some of its massive Mortgage Backed Securities holdings. This is important to anyone looking to purchase or refinance a home. That’s because this announcement immediately pushed Bond prices significantly lower, as Traders tried to get their own positions sold. Think of it as a financial game of musical chairs... in which no one wants to be the last one standing with a mitt full of Mortgage Backed Securities. This isn’t the last we’ll hear about this - and since home loan rates are tied to Mortgage Backed Securities, this creates the potential for home loan rates to rise in the near future. Fortunately, home loan rates are still at very attractive levels for now, despite the Bond market taking a hit for most of last week. So if you’ve been thinking about purchasing or refinancing a home, this is the time to see how you can benefit before rates possibly move higher. Because as bad as it was to lose some Bond pricing in the last few days, prices could move significantly worse depending on how they hold on to technical support. For more information on what this means and how it may impact you or someone you know, call or email today. I’ll be happy to explain the situation and offer advice based on your unique situation. |

| Forecast for the Week |

|

|

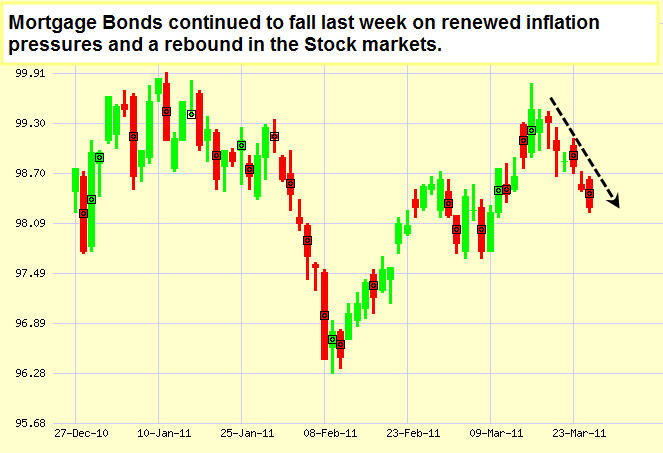

| This week will be busy from start to finish... but the biggest news will hit on Friday!

Remember: Weak economic news normally causes money to flow out of Stocks and into Bonds, helping Bonds and home loan rates improve, while strong economic news normally has the opposite result. As you can see in the chart below, Bonds and home loan rates took a negative turn last week, due in large part to pressure from inflation concerns and a rebound in the Stock market. However, rates are still attractive - making this an opportune time to take action for people looking to purchase or refinance a home before rates potentially worsen further. Chart: Fannie Mae 4.0% Mortgage Bond (Friday Mar 25, 2011)

|

| The Mortgage Market Guide View... |

|

|

| Safe Ways to Bank With Your Smart Phone Follow these steps to lower the risk of having your personal information stolen. By Cameron Huddleston, Kiplinger.com Using your smart phone to check your bank account balance or deposit a check is convenient. But is it safe? Hackers are getting better at finding ways to tap into smart phones and capture people’s account numbers and other personal information. However, there are ways to lower your risk of becoming a victim, says Michael Gregg, a cyber security expert and founder of Superior Solutions. Here are his tips: Don’t use public Wi-Fi to access accounts online. Use your phone provider’s network, instead, because it’s more difficult for hackers to tap into it. Public Wi-Fi connections, on the other hand, are easily compromised not just by savvy cybercriminals but by anyone who downloads a free program, which allows users to see what others are doing online and log onto their accounts as them. Watch out for smishing (fake text messages). If you get a text message supposedly from your financial institution warning you that there may be a problem with your account, don’t click on any links or call a number in the message. The link could take you to a phony site with malicious software that will give criminals access to your phone. And the number could connect you with scammers who are trying to collect your account information. Go directly to your bank’s Web site to check your account or to get a customer service number. And if you get a text message asking you to download a security update for your phone, don’t be fooled. Smart phone makers don’t send out security updates by text message, Gregg says. Be careful where you browse. Go to sites you know to conduct financial transactions. And before downloading any banking applications, check your financial institution’s site to make sure it offers one. Apple puts all apps for the iPhone through serious scrutiny, but other smart phone makers do not. A year ago, more than 50 fraudulent mobile banking apps appeared in the Android marketplace and were removed once they were discovered -- after many had bought and downloaded the apps. Don’t jailbreak your iPhone. You’ll lose your security mechanisms, Gregg says, if you tamper with your iPhone so it can run on another service provider’s network or download additional apps. Reprinted with permission. All Content ©2011 The Kiplinger Washington Editors. www.kiplinger.com.

Economic Calendar for the Week of March 28 - April 1, 2011 Remember, as a general rule, weaker than expected economic data is good for rates, while positive data causes rates to rise. Economic Calendar for the Week of March 28 - April 01

|