| |

|

| |

| | In This Issue  |

| | | | | | Last Week in Review: There was plenty of news for both optimists and pessimists last week. Find out what that meant for home loan rates. Forecast for the Week: Big job news is ahead, but will it be positive or negative? View: Changes are coming from Fannie and Freddie in 2012. Get the scoop below! | | | | | |

| | Last Week in Review |

|

|

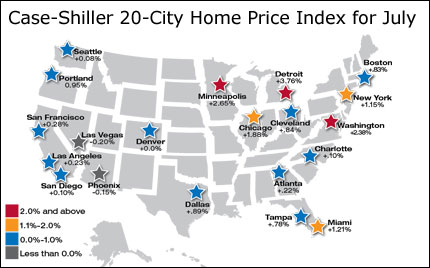

| | | | | | “Both optimists and pessimist contribute to our society. The optimist invents the airplane, and the pessimist—the parachute.” G.B. Stern. And last week, we saw sentiment on the economy go from pessimistic, to optimistic, and back to pessimistic—all within a week! Here are the highlights of what happened.  On the optimistic side, several economic reports were better than expected. For example, New Home Sales for August were up 6.1% from a year earlier and the Case-Shiller Home Price Index rose in July from June in the 10 and 20 city survey, and was the fourth monthly gain in a row. On the optimistic side, several economic reports were better than expected. For example, New Home Sales for August were up 6.1% from a year earlier and the Case-Shiller Home Price Index rose in July from June in the 10 and 20 city survey, and was the fourth monthly gain in a row. What’s more, there was some positive news from overseas. European leaders are designing a Special Purpose Vehicle (SPV) that would issue Bonds and purchase European debt to try to contain the malaise in that region. Plus, Germany voted in support for the expansion of the European Financial Stability Facility (EFSF), which will be used to help Euro member countries access capital. This is optimistic news, as it shows Germany is doing whatever it can to help debt laden countries avoid default and potentially threaten the Euro union. While this mix of news was great for our economy and the global economy, the result was a "risk on trade" where investors fled the safe haven trade of Bonds and moved into Stocks to try and take advantage of gains. And since home loan rates are tied to Mortgage Bonds, when Bonds worsen home loan rates worsen as well. That’s what we saw happen in the early and middle part of last week. But some pessimism crept back into the markets late last week as China's Manufacturing PMI contracted for a third consecutive month. There is growing fear that a slowdown in China could affect the already fragile global economy. This is a developing story and one I will be watching closely because if China’s economy does meaningfully slow, it will likely take Stocks down another level and help Bonds and home loan rates. Also creating some pessimism late in the week: Personal Income was lower than expected, and seeing earnings contract is not a good sign for the economy. The bottom line is that now is a great time to purchase or refinance a home, as home loan rates remain near historic lows. Let me know if I can answer any questions at all for you or your clients. | | | | | |

| | Forecast for the Week |

|

|

| | | | | | Can the U.S. job market get back on its feet? We’ll find out this week, along with more manufacturing news: - On Monday, the ISM Index will be delivered, and it’s probably the most closely watched manufacturing report out there.

- Jump ahead to Wednesday to see the first labor market reading of the week with the release of the ADP Employment Report.

- Weekly Jobless Claims will be released as usual on Thursday. Last week's drop below 400,000 was welcomed by investors, but the Labor Department said the numbers were somewhat impacted by seasonal adjustment factors.

- Last but not least is Friday's Jobs Report, which includes Hourly Earnings, Average Workweek, Unemployment Rate and the closely watched Non-farm Payrolls Report. In August, there were zero jobs created, which was a major blow to the psyche of the investment world. So the markets will be watching this report closely.

Remember: Weak economic news normally causes money to flow out of Stocks and into Bonds, helping Bonds and home loan rates improve, while strong economic news normally has the opposite result. As you can see in the chart below, Bonds and home loan rates were able to remain above a key trading level. I’ll be watching closely to see which way sentiment impacts the markets this week. Chart: Fannie Mae 3.5% Mortgage Bond (Friday Sep 30, 2011) | | | | | |

| | The Mortgage Market Guide View... |

|

|

| | | | | | | | | | | | | | Fannie and Freddie to Increase Fees…

But What Does It Mean? Starting in 2012, Fannie Mae and Freddie Mac are expected to increase their fees, which could impact homebuyers depending on the risk of their loan or the location of their home. Here’s what you need to know – including what’s really happening and what it means to homebuyers. What fee is being increased? First, it’s important to remember that Fannie Mae and Freddie Mac do not actually make home loans. Instead, they provide financing to lenders by purchasing mortgages from those lenders. Then, Fannie and Freddie either keep those mortgages on their books or they package them (in the form of securities) for sale to investors. That means, Fannie and Freddie don’t actually charge direct fees to homebuyers. But they do charge fees to lenders when they purchase home loans from those lenders. The lenders, in turn, build those fees into the home loans they offer. So the bottom line is that any increase in the fee that Fannie and Freddie charge lenders will essentially be passed on to consumers. However, the fees likely won’t be increased the same amount across the board. For example, Fannie and Freddie may charge higher fees when purchasing riskier loans or they may vary the fees based on which part of the country the home is located in (taking into account things like the foreclosure rate of the location). Why is this happening? Fannie and Freddie were seized by the government three years ago to help protect them from failing. That’s important because Fannie and Freddie (along with other government agencies) actually guarantee about 9 out of every 10 new home loans—and with the challenges that the housing market has seen recently, those guarantees have been extremely important. However, Fannie and Freddie have also cost the taxpayers more than $140 Billion. So Fannie and Freddie will gradually increase their guarantee fees next year and reduce the size of the home loans they purchase in an effort to: 1. Save tax | |

Posted via email from philipjensen's posterous

No comments:

Post a Comment